|

Post 12 – Art for the Hagler Institute For Advanced Study

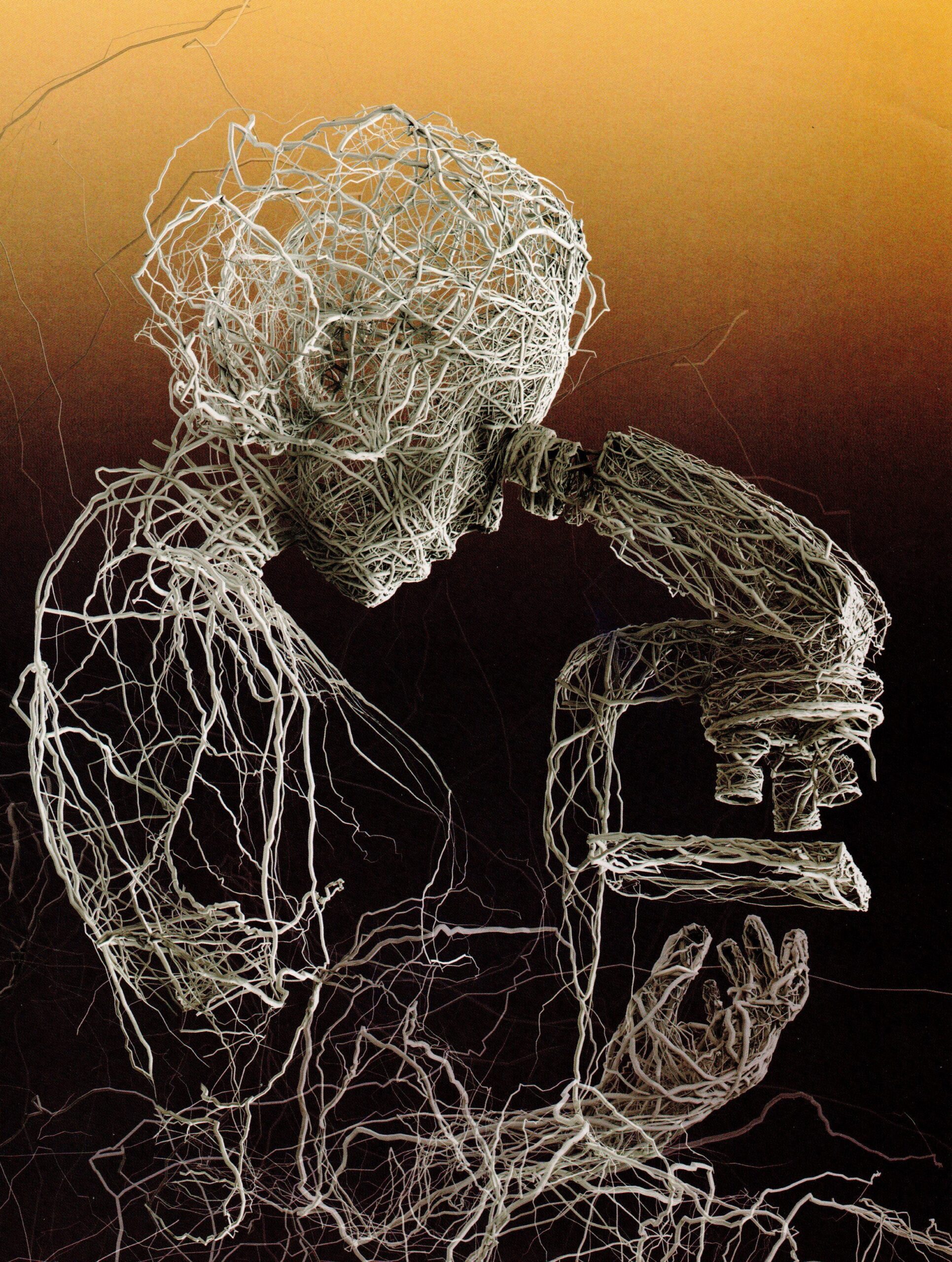

One of my favorite quotes about art is by Alberto Giocometti, a 20th century Swiss sculptor and painter. He said, “The object of art is not to reproduce reality, but to create a reality of the same intensity.”

One intense endeavor is the search for new knowledge. I never thought much about what kind of art would portray this search, but it “plopped in my lap”, as the old saying goes. Three drawings now hang on a wall outside my office that capture the intensity of the quest for new knowledge.

The art came from the A&M Foundation, that raises major donations and estate gifts for Texas A&M University. The drawings appeared in a feature story about the Hagler Institute for Advanced Study in the Foundation’s magazine, Spirit.

I have loved these pieces of art since I first saw them, and I want to share them with you in this post. They are best seen on a computer monitor.

A little background is helpful. I am Associate Director of the Hagler Institute. The Institute brings world-class researchers, called Fellows, to Texas A&M for from three to twelve months to collaborate with our faculty and students. These relationships foster an enrichment of ideas and solutions to tough problems. Texas A&M is good place for these Fellows to work, as it is the largest research institution in Texas at $1.153 billion dollars in research funds (2022 data).

Briefly, here is the way the institute works. The institute gives each college at Texas A&M the same basic allotment of nominations. Any member of A&M’s faculty can nominate a scholar located anywhere in the world with whom they would like to collaborate. On a two-page form the nominator describes the nominees’ accomplishments and explains the importance of having that person at Texas A&M. Because there are resource implications, the college deans forward the nominations to the institute and agree to our policies.

The nominations, which are secret, go to a revolving committee of nine University Distinguished Professors, who evaluate the nominees over several months to ensure they meet the high standards of the institute. If you are a scientist, for example, you must be in the National Academy of Sciences to be considered. The nominee must also demonstrate an ability to work with others and be currently productive. These high standards enhance the prestige of being chosen for the Hagler Institute.

The institute’s staff helps recruit the approved nominees. Once a Fellow is recruited, the institute pays 70% of his or her compensation. It also provides two fellowships to Ph.D. students (per Fellow), allowing students to work with Fellows and their hosts. The nominating college pays the remaining 30% of the compensation, as well as the cost of travel and housing.

I joined the institute after its first year of operation, and I have worked there for ten years. During that time, we have brought to A&M more than 100 of the world’s finest scholars, in everything from Shakespeare studies to quantum theory. We attract a new group of Fellows each year. Although the institute was not designed as a recruiting arm for A&M, 23% of Fellows have joined A&M’s faculty after completing their time in the institute.

The institute has brought in several Nobel Prize winners, a three-time recipient of the State Prize of Russia, awardees of the National Medal of Science, the National Humanities Medal, many recipients of prestigious research honors, and members of U.S. national academies and exclusive academies around the world.

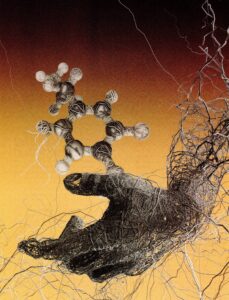

With that background I invite you to now enjoy three pieces of art used by the A&M Foundation for their 2017 “Great Minds” Spirit article about the Hagler Institute for Advanced Study.

Aren’t these just “too cool?”

Post 11 – Prior Posts and the Federal Debt

|

|||||

|

Post 10 – Inflation

Post 10 – Inflation

“By a continuing process of inflation, government can confiscate, secretly and unobserved, an important part of the wealth of their citizens.” —John Maynard Keynes

“It is a way to take people’s wealth from them without having to openly raise taxes. Inflation is the most universal tax of all.” —Thomas Sowell

Prices are the exchange rates between money and goods and services. If rates of money growth exceed growth rates in the production of goods and services, prices will rise.

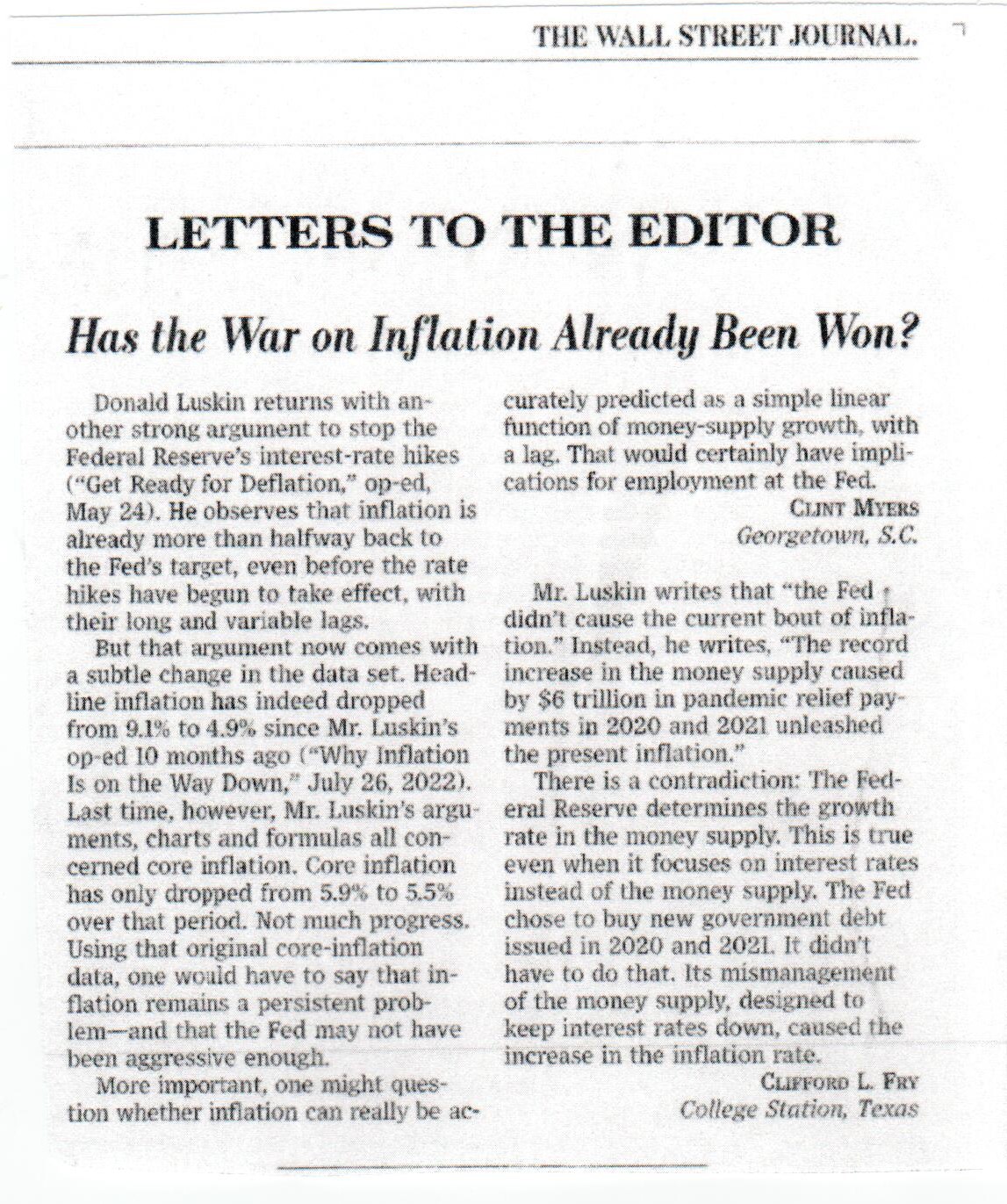

Inflation refers to a persistent increase in prices. Inflation is caused by too rapid growth in the money supply. Since the Federal Reserve controls the money supply, inflation is caused by the Federal Reserve.

When I was in graduate school in economics, this connection between inflation and too rapid growth in the new money was so theoretically and empirically well-documented by Milton Friedman and others that any student forgetting this relationship would have failed. Astoundingly, the current Federal Reserve leaders, to our detriment, are incorrectly focusing on interest rates rather than on money growth. There are economists who are trying to call attention to this. One is Professor Steve Hanke of Johns Hopkins University, and you can see him discuss these issues at

Inflation Just Got Lower, What’s Next? Economist Steve Hanke’s 2023 Forecast – YouTube

Inflation is different than increases in prices due to a key input, such as energy, becoming more expensive. Once prices adjust to the more costly input, price increases stop.

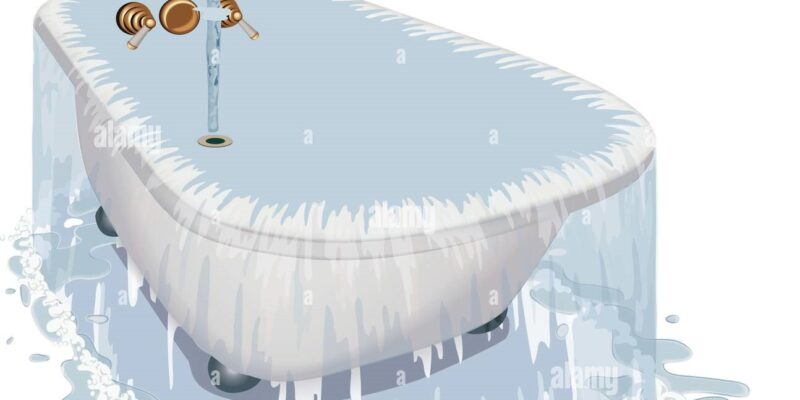

Prices do not stop rising during an inflation. For an analogy, consider water going into a bathtub that is full (economy at full rate of production) at the same rate that water drains from it. The bathtub will remain full of water. However, if you increase the rate of water (money) inflow, then water will overflow the tub and cause damage (inflation).

Unless other policies interfere, if the economy is not at maximum production (bathtub is not yet full), an increase in money (water) growth will induce real production to expand until it cannot increase any faster (until the tub is full). At that point any higher growth rate in the money supply will translate into a higher inflation rate (overflow). An inflation rate will persist as long as the accompanying rate of growth in the money supply persists.

When I was a professor at the University of Houston during the late 1970s and 1980’s, I co-authored an article in the Journal of Finance demonstrating that a quarterly increase in the money supply (M2) will influence the dollar volume of national output each quarter for about two years. This impact over time results from the new money circulating through the economy. Assessing the lagged effects are tricky because future variations in the money supply will also be influencing the economy during the impact periods of earlier changes.

Here is the source of current inflation. In the year ending January 1, 2020, the M2 money supply had grown at a 6.69% annual rate. The Biden administration, which came into office at that time, increased government spending by 67% in one year, some due to sending people money during the Covid lockdown. This spending was financed by borrowings through issues of government securities. The Federal Reserve chose to buy a heavy portion of these securities, injecting new money into the economy, rather than allowing interest rates to increase with the borrowing. I said as such in the Wall Street Journal, May 30, 2023 issue.

The Federal Reserve increased the money supply in the first five months of 2020 at a rapid rate. Its growth rate for the year ending May 2020, only five months later, had increased to 22%, and for each of the next ten months money grew from a year earlier at greater than a 20% pace. The “tub” was overflowing.

Here is a broader view. The two-year average growth rates in the M2 money supply ended January 1 for 2018, 2019, and 2020, respectively, are 5.59%, 3.18%, and 5.18%. The two-year averages for the consumer price index ending the same periods are 2.13%, 2.37%, and 1.87%.

For the two-years ended 2021, 2022, and 2023, the money supply growth rate was 19.52%, 16.27%, and 4.66%, respectively. The slowing for the two-years ended January 1, 2023 was due to reductions in the money supply in late 2022. Declines in the money supply are continuing as I write (mid-2023), The two-year inflation index for the same periods are 1.26%, 4.96%, and 7.87%, respectively. Note the lag in the impact of the rapid money growth on the inflation rate.

Due to lagged impacts, the inflation rate will likely decline to the 3-5% range for 2023. Since prices are not perfectly flexible downward, when money growth is abruptly decreased the real output growth in the economy will likely decline, also. The abrupt slowing in the two-year averages of money growth, from the high teens in 2021 and 2022 to 4.66% for the two-years ending January 1, 2023, along with the declines in the money supply during 2023, raise the prospect not just of slower economic growth but of a recession.

The government requires us to hold our retirement funds in liquid assets, such as cash, short term securities, bonds, or stocks. This is why inflation so easily damages our retirement funds. Unless our rate of earnings on financial investments exceeded the inflation rates in recent periods (if yours did not, don’t feel alone), our retirement funds have decreased in purchasing power during that time. For example, over the last two years, your rate of earnings on financial assets had to be 7.87% per year to maintain purchasing power.

Government finances its debt with new money (don’t you wish you could??) and you and I pay in loss of purchasing power of our retirement funds. The same is true for our wages, interest earnings, and dividend income, if any of these apply.

“Inflation is taxation without legislation” —Milton Friedman

“Inflation destroys saving…” —Kevin Brady

Post 9 – Grief

|

||||||||

|

Courtesy Mary Forest Engel

Courtesy Mary Forest Engel

Courtesy Mary Forrest Engel

Courtesy Mary Forrest Engel Courtesy Mary Forrest Engel

Courtesy Mary Forrest Engel

Post 8 – Ashley and Henry

|

|||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||

|